The past few years have been a figurative roller coaster ride for the construction industry. As construction continues to confront things like a declining workforce and inflation, we’re likely to see a few more twists and turns this year. Agents will need to keep a watchful eye on industry trends and what current market conditions may mean for construction clients and their coverage needs.

Here are a few things to watch throughout the remainder of 2023:

1. Skilled Labor Shortage. The construction industry has been battling a dwindling labor force in recent years, and that’s not expected to change in 2023. Put simply, there aren’t enough skilled workers to fill the open construction jobs.

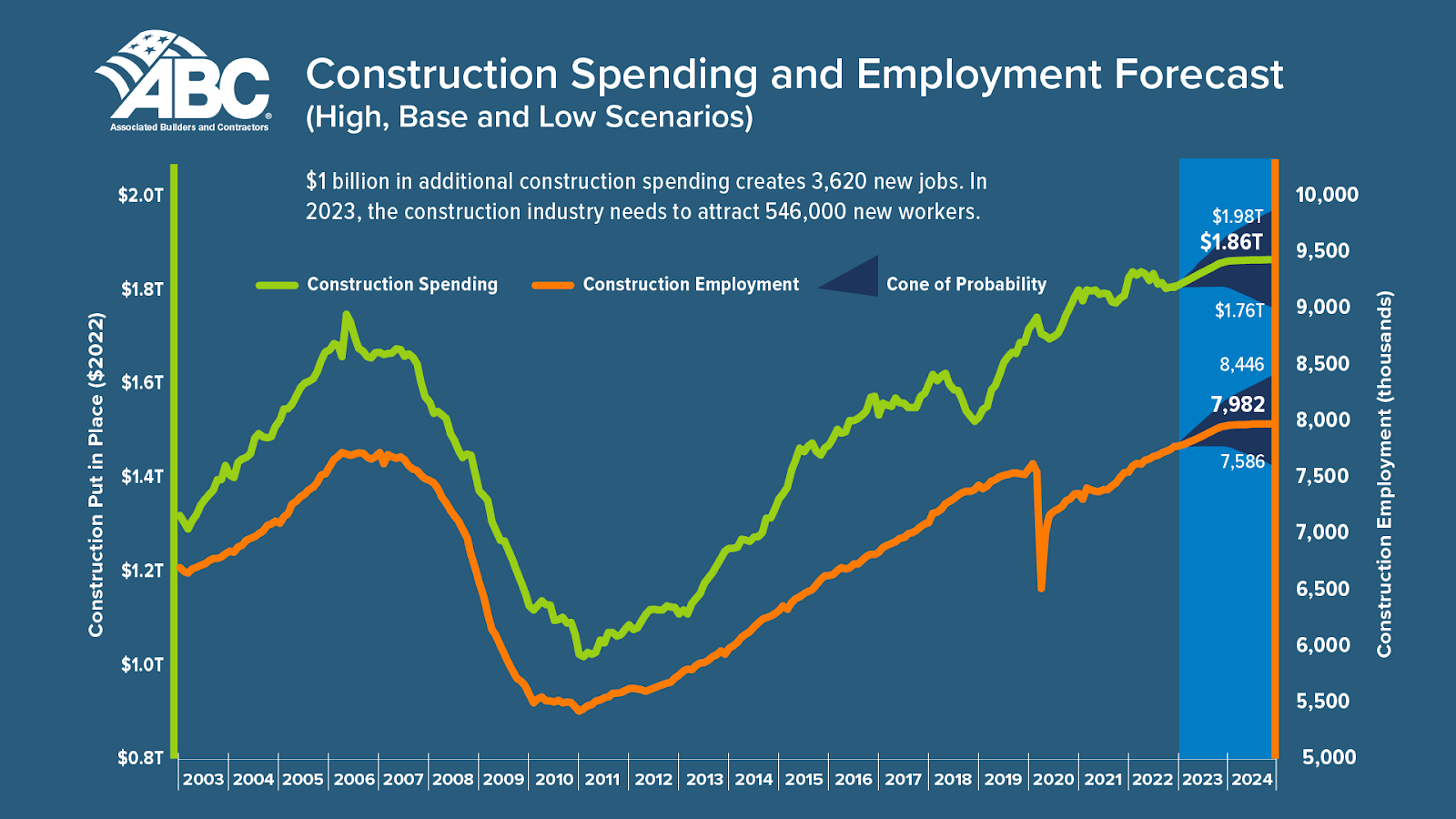

According to the U.S. Bureau of Labor Statistics, the average age for construction workers is 42.4 years old. As more Baby Boomers reach retirement, they leave gaps in the workforce that aren’t filled fast enough by up-and-coming talent. Associated Builders and Contractors estimates the industry needs over half a million additional workers on top of the typical hiring pace to meet project demands.

The impact of these labor shortages are broad-sweeping, resulting in things like project delays, poor workmanship, and increased builder risk. The industry is also forced to pay higher rates to attract and retain talent, which drives up total project costs.

According to Associated Builders and Contractors (ABC), we’ll need 546,000 additional construction workers to keep up with demand. (Source)

2. Worker Safety Concerns. Labor shortages can also impact worker well-being. Companies trying to close their labor gap by training and upskilling new talent are confronted by the risks inherent with a less-than-experienced workforce. Mistakes or poor judgment can increase on-the-job accidents and injuries. In addition, construction companies are trying to do more with less, putting pressure on workers who may rush through work, take shortcuts, or commit to increased hours.

Now, more than ever, companies will have to prioritize safety programs to protect their workers, reduce liabilities, and minimize claim severity and frequency.

3. Inflation and rising costs. By now, everyone is growing weary of the topic of inflation, but unfortunately it’s a trend that will continue to impact construction throughout 2023. Inflation reached a 40-year high in 2022, impacting everything from building supply prices, equipment purchase and rental prices, and labor costs. The good news is that inflation has been falling in recent months, and construction material costs are seeing some relief as a result. However, prices across the board still remain high.

Very simply, from an insurance perspective, the higher the prices, the more a building costs to build, and the more it costs to insure.

4. Infrastructure building projects. At the end of 2021, Congress signed the $1.2 trillion Infrastructure Investment and Jobs Act. This bill allocated funding for commercial construction, including transportation, utilities, major infrastructure projects (e.g. roads and bridges), power infrastructure, and the electricity grid. The bill is expected to spur construction spending and boost demand for civil and infrastructure construction services.

In addition to the obvious benefits this may have for larger construction firms, this could also mean more joint venture opportunities for smaller contractors and construction companies who want to join forces to tackle larger projects. All these new projects, regardless of size, will prompt various coverage considerations—from Workers’ Compensation to General Liability and Excess Liability and more.

5. Growing Cyber Crime Threats. According to NordLocker, construction holds the #2 spot for being the most targeted industry for ransomware attacks between January 2020 and January 2022. Ransomware attacks, however, are just one of the many cyber crimes construction companies need to watch for in the coming year. As construction companies adopt more technology and tools to streamline operations and gain efficiencies (everything from better order management and customer portals to robotics and drones), the more vulnerable they become to attack and exploitation. Small and medium-size businesses are particularly at risk, because they often lack the resources and expertise to implement appropriate security measures.

Companies will need to be proactive and vigilant when it comes to protecting themselves against cyber risk. Without proper cyber security and risk mitigation, construction companies open themselves up to attacks that can expose company and customer data and result in everything from business interruptions and delayed projects to payment interception and compromised equipment.

Stay ahead of construction trends and their insurance implications by partnering with Jencap. Our unmatched market access and strong carrier relationships will give your clients the best coverage and rates available. Contact us today to get started.